BSc (Hons), MSc • Lifelong Learner Award 2008 • Personal Brand Award 2017 • 2025 Spirit of Enterprise Honouree

Cayden Chang is the Founder of Mind Kinesis Investments Pte Ltd and Value Investing Academy Pte Ltd, home to Asia’s first and only Value Investing programme endorsed by Mary Buffett, the internationally acclaimed author and speaker on Warren Buffett’s investment philosophy.

With over 50,000 graduates across 11 cities in Asia, Cayden’s methodology is tested, proven, and designed to be duplicable, even for those with no prior investing experience.

Cayden holds two Bachelor’s Degrees and a Master’s Degree from the National University of Singapore. He has been trained in value investing by Professor Bruce Greenwald at Columbia University (the same institution where Warren Buffett studied under Professor Benjamin Graham) and by Professor George Athanassakos, who holds the Ben Graham Chair in Value Investing at the Richard Ivey School of Business, University of Western Ontario.

Cayden has been featured across major Singapore and regional media, including The Straits Times, TODAY, Channel NewsAsia, 938Live Radio, The Edge, and Shareinvestment, among others.

In 2010, Cayden was diagnosed with terminal stage renal cancer (Stage 4). Despite his illness, he launched a charity initiative, donating all proceeds from his first book to The Straits Times School Pocket Money Fund. He survived and went on to face two further bouts of cancer by 2019.

Rather than withdraw, he channelled his experience into purpose. He launched the Cayden Chang Inspire Award, participated in the HCA Walk With Me Charity Walkathon, and continued teaching. His life story was featured in The Sunday Times under the headline ‘Losing $50k before wedding changed his life’ on 24 September 2017.

Today, his mission is to build an endowment fund for cancer research and hospice care, and to help as many investors as possible achieve financial independence so they can care for the people they love.

“I didn’t want anyone else to go through the same painful lessons I experienced. I care about making you a better, more confident investor.”

Cayden Chang

The following terms appear throughout this playbook. This reference is intended to give you working definitions in plain language — the way these concepts are actually used by practising value investors.

All-Weather Portfolio

A portfolio constructed to perform reasonably well across different market conditions — rising markets, falling markets, high inflation, and low growth. Typically combines stocks, bonds, and other asset classes so that gains in one area offset losses in another.

Annualised Return

The average yearly return of an investment, expressed as a percentage, calculated over a multi-year period. Allows fair comparison between investments held for different lengths of time. For example, the S&P 500's annualised return since 1965 has been approximately 9.9% with dividends reinvested.

Bear Market

A market condition in which prices fall 20% or more from recent highs, typically accompanied by widespread pessimism. Historically, every bear market has eventually been followed by a recovery. Value investors treat bear markets as opportunities to acquire quality businesses at discounted prices.

Bull Market

A sustained period of rising asset prices, typically defined as a gain of 20% or more from recent lows. Bull markets are generally associated with economic expansion, investor confidence, and growing corporate earnings.

Cash-Flow Options Strategies (CFOS)

An investment approach that involves selling options contracts on fundamentally strong, undervalued companies in order to collect upfront premium income. CFOS generates consistent cash flow regardless of short-term market direction, and can be used to either earn returns without owning a stock or to acquire quality businesses at a further discount. Modelled on principles used by Warren Buffett. Higher market volatility typically increases the premiums available.

Competitive Moat (Economic Moat)

A durable competitive advantage that protects a business from rivals over the long term — analogous to the moat that surrounds a castle. Examples include strong brand recognition, network effects, proprietary technology, cost advantages, and high customer switching costs. A wide moat is a key indicator of intrinsic value stability.

Compounding

The process by which investment returns generate their own returns over time. Often called the 'eighth wonder of the world', compounding accelerates wealth growth the longer it is allowed to run. Reinvesting dividends is one of the most powerful ways to harness compounding.

Conviction

The process by which investment returns generate their own returns over time. Often called the 'eighth wonder of the world', compounding accelerates wealth growth the longer it is allowed to run. Reinvesting dividends is one of the most powerful ways to harness compounding.

Discount to Intrinsic Value

The difference between a stock's current market price and its calculated intrinsic value, when the price is lower than the value. Buying at a discount is the core objective of value investing. The larger the discount, the greater the potential return and the larger the margin of safety.

Diversification

The practice of spreading investments across different companies, sectors, asset classes, or geographies to reduce the impact of any single investment's poor performance on the overall portfolio. Diversification manages but does not eliminate risk.

Dividend

A portion of a company's profits distributed to shareholders, typically on a regular schedule. Reinvesting dividends — using them to purchase additional shares rather than receiving cash — significantly amplifies long-term returns through compounding.

Dollar-Cost Averaging (DCA)

An investment strategy that involves investing a fixed amount of money at regular intervals, regardless of market conditions. When prices are high, the fixed amount buys fewer units; when prices fall, it buys more. Over time, this lowers the average cost per unit and removes the need for market timing.

Due Diligence

The thorough research and analysis a prudent investor conducts before making an investment decision. In value investing, due diligence typically involves examining financial statements, understanding the business model, assessing the competitive position, evaluating management quality, and calculating intrinsic value.

Economic Cycle

The natural rise and fall of economic activity over time, moving through phases of expansion, peak, contraction, and trough. Investment markets broadly follow economic cycles — periods of growth (bull markets) give way to slowdowns (bear markets) and vice versa. Long-term investors benefit by remaining invested across cycles.

ETF (Exchange-Traded Fund)

A type of investment fund that holds a basket of assets — such as stocks, bonds, or commodities — and trades on a stock exchange like a single share. Index ETFs, such as those tracking the S&P 500, offer broad market exposure at low cost and are a cornerstone of the Dollar-Cost Averaging strategy described in this playbook.

Fundamental Analysis

The method of evaluating a business by examining its financial statements, earnings, revenue, profit margins, debt levels, competitive position, and management quality to determine its intrinsic value. The primary analytical tool of value investors, as distinct from technical analysis which focuses on price charts.

Fundamentals

The method of evaluating a business by examining its financial statements, earnings, revenue, profit margins, debt levels, competitive position, and management quality to determine its intrinsic value. The primary analytical tool of value investors, as distinct from technical analysis which focuses on price charts.

Index Fund

A type of investment fund designed to replicate the performance of a specific market index, such as the S&P 500. Index funds offer broad diversification, low fees, and consistent market-rate returns. Warren Buffett has publicly recommended them for most investors.

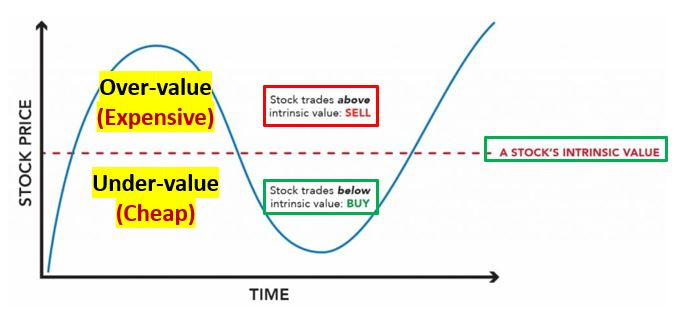

Intrinsic Value

The true underlying worth of a business, based on its fundamentals — earnings power, assets, competitive position, and growth prospects — rather than its current market price. Intrinsic value is calculated through analysis and remains more stable than daily share prices. The goal of value investing is to buy shares at a price below intrinsic value.

Margin of Safety

The gap between a stock's purchase price and its calculated intrinsic value. Originally articulated by Benjamin Graham, the margin of safety acts as a buffer against errors in analysis and unexpected business setbacks. A larger margin of safety means lower risk and greater potential return.

Market Capitalisation

The total market value of a company's outstanding shares, calculated by multiplying the current share price by the number of shares in issue. Market capitalisation is a measure of market perception, not intrinsic value — the two can diverge significantly.

Market Sentiment

The overall attitude or mood of investors toward the market or a particular security, driven by news, emotions, and crowd psychology rather than fundamental analysis. Sentiment can cause prices to diverge sharply from intrinsic value — creating both overvalued and undervalued conditions that value investors seek to exploit.

Market Timing

The overall attitude or mood of investors toward the market or a particular security, driven by news, emotions, and crowd psychology rather than fundamental analysis. Sentiment can cause prices to diverge sharply from intrinsic value — creating both overvalued and undervalued conditions that value investors seek to exploit.

Options Contract

A financial instrument that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a specified price before a specified date. In Cash-Flow Options Strategies (CFOS), the seller of an options contract receives an upfront premium in exchange for taking on an obligation. Selling options on quality businesses at attractive prices is a core CFOS technique.

Premium (Options)

The price paid by the buyer of an options contract to the seller, received upfront regardless of what happens to the underlying stock. In volatile markets, premiums are higher — which is why CFOS practitioners can collect more income during periods of market uncertainty.

Price-to-Value Ratio

An informal measure comparing a stock's current market price to its estimated intrinsic value. When price is below intrinsic value, the stock is considered undervalued (a potential buying opportunity). When price is above intrinsic value, the stock is considered overvalued (a potential selling opportunity).

QQQ (Nasdaq-100 ETF)

An exchange-traded fund that tracks the Nasdaq-100 index, comprising the 100 largest non-financial companies listed on the Nasdaq. Heavily weighted toward technology companies. Referenced in this playbook as a real-world example: Cayden purchased QQQ shares during the April 2025 market sell-off, generating a 19.7% gain in 23 days by applying value investing principles.

S&P 500

The Standard & Poor's 500 index, tracking the 500 largest publicly traded companies in the United States. Widely considered the benchmark for U.S. stock market performance. Since 1965, the S&P 500 has delivered an annualised return of approximately 9.9% with dividends reinvested — surviving the Great Depression, Black Monday, the dot-com crash, the Global Financial Crisis, and the COVID-19 pandemic.

Share Price

The current market price at which a single share of a company can be bought or sold on a stock exchange. Share price is determined by supply and demand, and reflects the collective sentiment of all buyers and sellers at a given moment. It frequently diverges from intrinsic value — this divergence is the core opportunity in value investing.

Speculation

The practice of buying or selling assets based primarily on expected short-term price movements, rather than on analysis of underlying business value. Speculators react to headlines, price trends, and market sentiment. Contrasted throughout this playbook with investing, which focuses on fundamental value and long-term business ownership.

Supply and Demand

The basic market forces that determine price at any given moment. When more investors want to buy a stock than sell it, the price rises; when more want to sell than buy, the price falls. Supply and demand explain short-term price movements, but over the long term, a company's financial performance is the dominant driver of price.

Value Investing

An investment philosophy, originally developed by Benjamin Graham and refined by Warren Buffett, that focuses on buying shares of fundamentally sound businesses at prices below their intrinsic value. Value investors conduct thorough research, maintain a margin of safety, think like business owners, and hold for the long term — profiting as the market eventually recognises the true worth of undervalued companies.

Volatility

The degree to which the price of an asset fluctuates over time, measured by the magnitude of price swings. A stock or index that moves sharply up or down is said to be highly volatile. Volatility is often mistakenly equated with risk. As this playbook explains, volatility and risk are distinct: volatility creates opportunity for the prepared investor, while risk is the product of insufficient knowledge about what you own.

- Robert J. Shiller: Nobel Prize in Economic Sciences (2013): nobelprize.org

- Benjamin Graham: The Intelligent Investor (Goodreads quotes): goodreads.com

- Morningstar: Why Investors Missed Out on Fund Returns: morningstar.com

- U.S. Securities and Exchange Commission: Luckin

Coffee Agrees to Pay $180 Million Penalty to Settle Accounting Fraud Charges: sec.gov/newsroom/press-releases/2020-319

Cayden Chang, Founder, Mind Kinesis Value Investing Academy

78 Shenton Way, AIG Building #05-02, Singapore 079120

enquiries@mindkinesis.com • +65 6438-7010 • www.viaatlas.com

© 2026 Mind Kinesis Value Investing Academy. All Rights Reserved.